EBITD Definition & Formula

Earnings before interest, tax and depreciation (EBITD) is a pre-tax measure of a company's operating performance. Essentially, it's a way to evaluate a company's performance without having to factor in many financing decisions, accounting decisions, or tax differences.

EBITD is calculated by adding back the non-cash expenses of depreciation to a firm's operating income and then adding back taxes. EBITD is not the same as EBITDA (EBITDA adds back amortization).

The formula for EBITD is:

EBITD = EBIT + Depreciation + Taxes

How to Calculate EBITD

EBITD is calculated using the company’s income statement. It is not included as a line item, but can be easily derived by using the other line items that must be reported on an income statement.

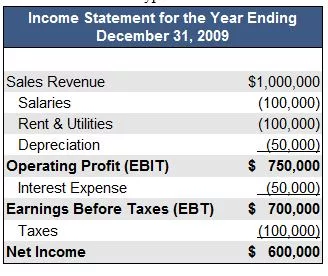

Let's take a look at a hypothetical income statement for Company XYZ:

As you can see, Company XYZ does not have any amortization (any many companies don't). Using the formula above, Company XYZ's EBITD is:

EBITD = $750,000 + $50,000 + $100,000 = $900,000

EBITD vs EBITDA

EBITDA is one of the operating measures most used by analysts, but EBITD is far less popular. Though EBITD does not factor in the direct effects of financing decisions, making it easier to compare companies' operating performance, it does not factor in the tax consequences of those decisions. It also excludes any amortization associated with intellectual property such as trademarks and patents, which may be a useful strategy for analysts interested in comparing the asset performance of companies. This in turn allows investors to focus on operating profitability as a singular measure of performance. Such analysis is particularly important when comparing similar companies across a single industry, and it is more useful for companies operating in different tax brackets. It is less useful, however, when comparing companies with different levels of intellectual capital.

EBITD, like EBITDA, can be deceptive when applied incorrectly. It is especially unsuitable for firms saddled with high debt loads, those that must frequently upgrade costly equipment, and those involving a lot of intellectual capital. Furthermore, EBITD can be trumpeted by companies with bad tax strategies in an effort to 'window-dress' their profitability. EBITD will almost always be higher than reported net income.

Also, because EBITD isn't regulated by GAAP, investors are at the discretion of the company to decide what is, and is not, included in the calculation from one period to the next. Therefore, when analyzing a firm's EBITD, it is best to do so in conjunction with other factors such as capital expenditures, changes in working capital requirements, debt payments, and, of course, taxes.