What Is a Money Market Account?

Money market accounts are a type of savings account that can be opened at any bank or credit union. Money market accounts usually offer higher interest rates than checking accounts and also allow individuals to write checks and use a debit card.

According to Andrew Denney, CEO of Prosperity Financial Group, money market accounts are a “very safe way to get good returns.” That’s because they’re insured by the Federal Deposit Insurance Corporation (FDIC) when issued by a bank and the National Credit Union Administration (NCUA) when issued by a credit union.

If you’re looking for a low-risk hybrid account to park your funds, a money market account may be right for you.

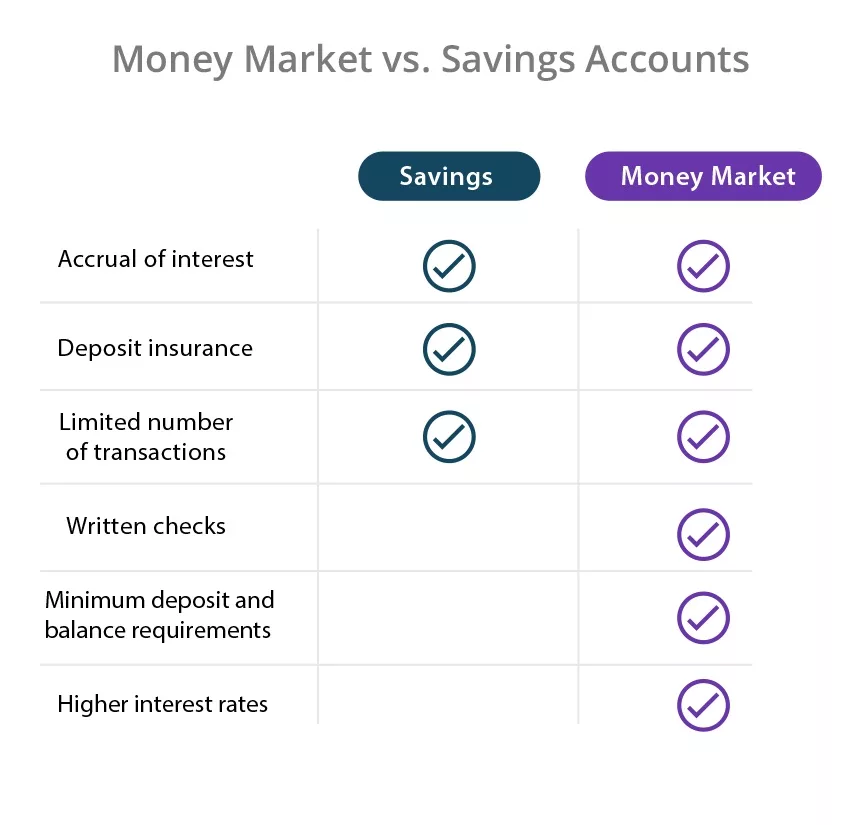

Money Market vs. Savings Accounts

Similarities:

Accrual of interest: Both accounts can offer interest rates higher than checking accounts.

Deposit insurance: Most major banks offer both accounts with FDIC insurance, which insures funds for up to at least $250,000.

Limited number of transactions: According to Regulation D of the Federal Reserve, the total number of transactions you can make is limited to six per month or account cycle.

Differences:

Written checks: Many money market accounts allow customers to withdraw money by check, unlike savings accounts.

Minimum deposit and balance requirements: Money market accounts are more likely to require specific minimum deposits to open. They also typically have higher minimum balance requirements.

Higher interest rates: Many banks offer slightly higher interest rates for their money market accounts than savings accounts.

If you are trying to decide between the two accounts, read more to determine whether a money market account or savings account is better for you.

What Are the Pros of a Money Market Account?

Money market accounts offer significant advantages like government-backed insurance, easy transactions, and interest rates that are higher than typical checking accounts.

Fully Insured

You can feel safe knowing that money market accounts offer FDIC insurance for up to at least $250,000. When using a credit union money market account, similar insurance exists from the NCUA. In the unlikely event that the bank or credit union goes out of business, your insured money will typically be reimbursed the next business day.

Transactions Are Easy

Many money market accounts include debit cards and checks so you can make purchases in the same way as traditional checking accounts. Most brick-and-mortar banks also offer an unlimited number of ATM – as well as in-person – withdrawals.

Competitive Interest Rates

In many cases, money market accounts offer comparable (or even higher) interest rates than savings accounts. For example, CIT Bank’s money market account offers 1.80% annual percentage yield (APY) compared to its Premier High Yield Savings (which only offers 1.55%).

Money market account interest rates are often lower with smaller balances but may increase if you reach a certain account balance. For example, Capital One’s 360 Money Market account offers an interest rate of 0.85% for balances up to $9,999, but that increases to 1.50% for balances greater than $10,000.

To get the best interest rates, it’s always a good idea to compare the money market accounts and savings accounts you qualify for.

What Are the Cons of a Money Market Account?

Some disadvantages of money market accounts include a capped number of monthly transactions, minimum opening deposit requirements, and monthly service fees.

The Number of Transactions per Month is Limited

Unlike checking accounts, which usually allow you to make an unlimited number of transactions, money market accounts are often limited to six per month (or single account cycle).

These types of transactions include:

Debit card transactions

Electronic funds transfers (EFTs)

Outgoing wire transfers

Automated Clearing House (ACH) withdrawals

Checks written to a third party

If you exceed the maximum number of six transactions in a statement cycle, you may have to pay a fee. For example, BMO Harris’s Platinum Money Market account charges a $15 fee per excessive transaction. To avoid excess charges, be mindful of this limit or use a checking account for the majority of your transactions.

Minimum Opening Deposits and Monthly Service Fees May Apply

Many money market accounts require a high minimum opening deposit, however, they often offer a higher interest rate.

For example, Popular Community Bank offers a 1.70% APY and requires a minimum of $10,000 to open an account. It also charges a $15 service fee if the average balance falls below that number. Therefore, it’s best to open a money market account if you plan on keeping your funds above the minimum balance to avoid any fees.

Money Market Calculator

To calculate the amount of money you’d earn by investing in a money market account, you’ll need the following numbers:

Your initial deposit balance

The monthly amount you’ll deposit into this account

The APY of the money market account

The number of years you plan on investing

When you have the above information, you can simply input the numbers into a money market calculator to find out your potential earnings.

How Are Money Market Rates Determined?

The Federal Reserve determines money market account rates. If the Federal Reserve increases the federal funds rate, money market accounts generally increase their rates as well.

Conversely, when the federal funds rate drops, your interest rate may do the same. Sometimes, banks may lower the amount of APY offered by money market accounts in anticipation of a federal funds rate cut.

How to Find the Best Money Market Accounts

When comparing different money market accounts, look out for the following information:

APYs: The highest APY will net the most money (as long as you meet any requirements to avoid fees).

Minimum balance requirements: Some banks or credit unions require a minimum deposit amount to open an account, and they’ll even charge a fee if you go below that amount.

ATM card access: Some accounts do not allow you to access ATMs for quick cash withdrawals.

Check writing: If you want to write third-party checks, make sure your bank provides this feature.

Physical presence: Avoid online-only banks if you want a physical to manage your funds.

What Are Average Money Market Rates in 2020?

The FDIC calculated the national average APY for money market accounts with deposits less than $100,000 at 0.16%. Accounts larger than $100,000 were estimated at 0.28%. While these numbers may seem low, you can find many higher-yield accounts that pay slightly less than 2% interest.

Is a Money Market Account Right For Me?

Choosing between a money market account or depositing your funds into a savings account, checking account, certificate of deposit, or municipal bond depends on your needs and goals. Consider a money market account if you’re looking for the following:

A hybrid account that consolidates a checking and savings account into one (which is useful if you don’t need a lot of transactions).

An easy-to-access account to store large funds (e.g. emergency fund, school tuition).

An FDIC-insured savings account with a debit card and checking features.

A low-risk, high-interest rate solution to avoid market volatility or help beat inflation.

An account to save money for a future expense (e.g. vacation, car purchase).

Generally speaking, opening a money market account is a low-risk, high-interest alternative to savings accounts. Since money market accounts are a hybrid between checking and savings accounts, their benefits and features are the best of both worlds.