Forget what you've heard, debt-laden companies offer great turnaround potential if you know what to look for.

For many investors, debt-free companies are the only way to go. They have the financial strength to withstand tough times, and in good times they can look to make deals, buy back stock or hike dividends. Yet for more intrepid investors, a company with high levels of debt can often deliver some of the strongest stock returns.

When the market crashed in 2008, high-debt companies like Hertz (NYSE: HTZ) and Delta Airlines (NYSE: DAL) saw their shares slump below $5. A number of their loans were up for renewal in coming quarters. If the economy worsened, and they couldn’t roll over that debt, then bankruptcy looked like a real possibility.

But as I'll explain, these types of stocks were also the strongest gainers when the market rebounded. Shares of Hertz and Delta both tripled from their early 2009 lows, and thanks to their continuing high levels of debt, could still be very strong gainers as the economy continues to improve. Here’s why.

Tax Savings & Anti-Dilution

At the end of the day, earnings, and more specifically, earnings per share (EPS), are the main reasons to own stocks. Even if investors assess companies by looking at their balance sheets, marketing savvy, global reach or a host of other factors, the most important metric for almost every investor is the bottom line. As per-share profits rise, companies are in a better position to boost dividends, attract fresh capital and pay off debt. And that's great for shareholders.

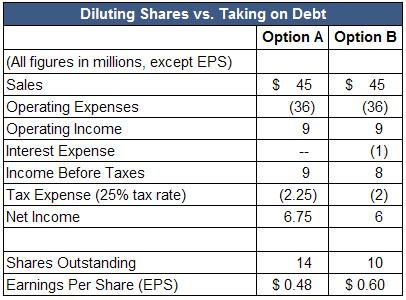

Let’s look at a company with 10 million shares outstanding and a $5 stock price. Assume the company wants to raise $20 million in fresh capital.

.webp)

One of its options is to issue new shares (Option A), which will dilute existing shareholders. To raise $20 million in new capital, the company has to sell 4 million shares at $5 each. That bumps the number of total shares to 14 million.

Earnings per share is determined by dividing profits by the total shares outstanding. So the more shares a company issues (which increases the denominator in the EPS calculation), the lower the earnings on a per-share basis.

Option B is to borrow the $20 million. Assuming the firm pays 5% interest per year, it adds $1 million in annual interest payments. Even so, Option B’s debt load allows the company to generate higher earnings per share. Let me explain.

Even though the additional interest payment leads to lower absolute profits ($4 million vs. $4.5 million), profit is higher on a per-share basis under Option B. Why?

First, because interest on debt is deducted before taxes are assessed, $1 million in interest income saves the company $500,000 in taxes. Second, by not adding 4 million new shares to the pool, earnings are split among fewer shareholders.

That’s why companies like GE (NYSE: GE) always carry large amounts of debt. If GE avoided debt, it would have issued far more shares than currently exist, and it would have lower earnings per share.

Using Leverage to Magnify Future Profit Growth

Debt (also known as leverage) can also magnify future profits. If the economy is stable or growing, taking on highly leveraged stocks is likely to pay off handsomely.

Let’s look at our company one year in the future and compare the performance of Option A to Option B. Let's assume sales have risen 50% and operating margins have stayed constant.

Under Option A, the company was able to boost EPS by $0.16, while Option B boosted EPS by $0.20. By using debt instead of equity, the benefit of increasing sales and increasing profits flows through to fewer shareholders, magnifying EPS.

How to Evaluate an Opportunity

So now you know that any time you hear a stock being derided for having high debt levels, you should think to yourself, 'This might be an opportunity!' If your research proves that the firm's debt concerns are manageable in the near term, you’re likely to profit as the company starts to use increased profits to chip away at their debt.

For the individual investor looking for opportunities, the trick is to make sure that debt-heavy companies generate ample cash flow to meet their annual interest expense and all near-term payments on loans. Near-term loan obligations are characterized as the 'current portion of long-term debt' detailed in notes to the company's financial statements. Companies are also required to disclose the maturity schedule of their long-term debt. A thorough understanding of how much a company owes and when it needs to repay its debt is vital to knowing the risk you're exposing yourself to.

Remember, this risky approach only works when the economy is stable or growing. But if the economy is shaky or looks to be headed south, you’d be better served by shedding any stocks with high debt loads.

[To learn how to evaluate companies using profitability, liquidity, and debt leverage ratios, click here to read 20 Key Financial Ratios Every Investor Should Use.]