Interest-Only Mortgage Calculator

Interest-only mortgages are considered high risk home loans and are not appropriate for all borrowers. But if you can qualify, and there’s a program available that meets your needs, it does have certain advantages.

To help you make that decision, we’re providing this Interest-Only Mortgage Calculator. You can use it to run loan scenarios and to help you better understand exactly how interest-only mortgages work.

How Does the Interest-Only Mortgage Calculator Work?

To use the Interest-Only Mortgage Calculator, you’ll need to provide only five pieces of information:

The loan Start Date – which is the day you expect to close on the mortgage.

Loan Amount – how much you are borrowing.

Enter the Loan Terms in Years (30 years or less) – this will generally be between 15 and 30 years.

Interest Rate per year – enter the rate you expect to pay on your interest-only mortgage.

Interest Only Period (in Years) – this is the number of years the loan will be interest-only; it will usually be five or 10 years.

Example of Interest-Only Mortgage Calculator

Let’s work an example to show how the Interest-Only Mortgage Calculator works.

We’ll enter the following information:

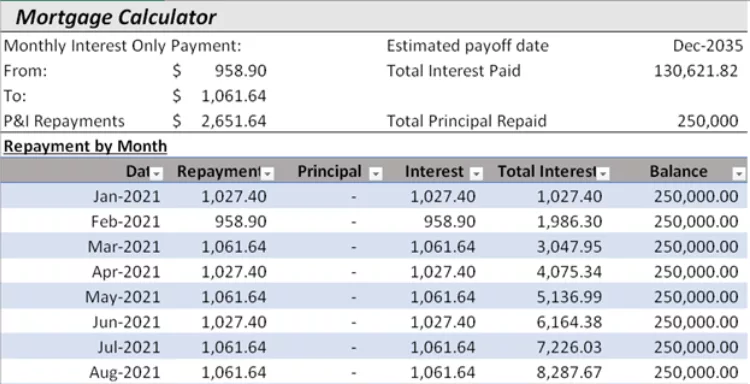

Start Date: January 1, 2021

Loan Amount: $250,000

Enter the Loan Terms in Years (30 years or less): 15

Interest Rate per year: 5%

Interest Only Period (in Years): 5

With that information, we get the following results:

The Interest-Only Mortgage Calculator provides the monthly interest payments in a range of $958.90 to $1,061.64.

The reason the payment is shown as a range is because it’s based on interest charged for the number of days in each month. While some months have 31 days, and others have 30, February has only 28 (and sometimes 29). The interest payment will vary somewhat each month.

The calculator also shows what your monthly payment will be once you begin making principal payments on the loan. At $2,651.64, the monthly payment will increase by more than 50% when principal repayment begins.

You’ll also see the cumulative amount of interest paid with each payment on the loan.

But that’s just the basic information the calculator provides. It will also display an amortization schedule. That will show what your payment will be each month, during both the interest-only period and during the principal repayment phase.

But you may also be interested to see the Repayment Table by Year. It displays the total amount of interest and principal you will pay each year of the loan until it’s paid in full.

If you prefer a visual representation, the calculator will also provide a bar chart showing how the repayment will look over the life of the loan.

What is an Interest-Only Mortgage?

As the name implies, an interest-only mortgage is one that requires only the payment of interest during the initial phase of the loan. You’ll make interest-only payments for the first few years of a loan-term, then begin making interest plus principal payments over the remaining term, until the loan is fully repaid.

The interest-only feature enables borrowers to have a lower monthly payment, which usually enables them to qualify for a larger mortgage on a higher priced home.

How Does an Interest-Only Mortgage Work?

Interest-only mortgages typically come in standard mortgage terms of between 15 and 30 years, though there are a few that will go as long as 40. By the end of the loan term, the principal balance will be fully repaid, no matter how the interest-only feature is structured.

The interest-only phase of the loan will usually run five or 10 years, based on the loan term. For example, the interest-only phase will be five years on a 15-year loan, and 10 years on a 30-year loan.

Once the interest-only phase ends, you’ll be required to make payments of both interest and principal over the remaining balance of the loan.

Because you haven’t made principal payments during the interest-only phase, the monthly payment will be dramatically higher once principal is added to the monthly payment.

This increase is largely due to the reduced term of the loan payoff. Instead of amortizing the principal on a 30-year loan over the full 30-year term, it will be paid in just 20 years. That will result in substantially higher payments than would’ve been the case if you had taken a standard fully amortizing loan.

Types of Interest-Only Mortgages

Like other mortgage programs, interest-only mortgages typically come in both fixed-rate and adjustable-rate varieties.

Fixed-rate interest-only mortgages usually come in terms ranging from 15 to 30 years. The interest-only period may be five years on a 15-year loan, and 10 years on a 30-year loan. In either case, the monthly payment will be the same throughout the interest-only period, and during the principal repayment phase (after principal repayment has been factored into the loan).

Adjustable-rate mortgages (ARMs) are much less standard. They can come with a fixed term of three, five, seven or 10 years, after which the loan will convert to either a six month or a one-year adjustable.

The interest-only period may apply only to the fixed term of the loan, though some lenders will extend it to 10 years on a 30-year mortgage. But if the interest-only phase extends beyond the fixed term, your interest rate will still adjust based on the formula disclosed in the loan documents.

Fortunately, ARMs come with what are known as “caps.” These are limits on the amount the interest rate can increase, both at the time of adjustment and over the life of the loan.

For example, an ARM may have caps of 2% for any single rate adjustment, and 5% over the life of the loan.

This means if your interest rate starts at 3%, it will rise by no more than 2% at the time of the first adjustment. Over the life of the loan, it cannot exceed 8% (the 3% initial rate, plus 5% on the lifetime rate cap).

These are just examples of the caps a lender might offer on an ARM. But since each ARM is a unique, in-house program, the lender can set caps they determined to be the most adequate.

Buyer Beware!

Details of ARM terms and caps will be given in the ARM program disclosure. Federal law requires lenders to provide this information on all loans. Be sure to read it carefully, and understand exactly what you’re signing up for.

Interest-only loans are risky enough with fixed-rate terms. But when you add ARM terms to the equation, the loans become even higher risk.

Interest-Only vs. Conforming Mortgages

Just a few years ago conforming mortgages offered an interest-only feature. But due to the rising foreclosures during the global financial meltdown (2007-8), the U.S. Government’s Consumer Financial Protection Bureau (CFPB) prohibited interest-only provisions on conforming loans in 2013.

That’s when interest-only and conforming mortgages became completely different loan types.

Conforming loans are those funded by the mortgage agency giants, Fannie Mae and Freddie Mac. Apart from FHA and VA mortgages (which also don’t permit interest-only provisions), Fannie Mae and Freddie Mac fund most of the mortgages issued in America.

Because they are federally chartered and regulated agencies, Fannie Mae and Freddie Mac impose various rules and regulations on lenders and the types of mortgages they can provide. Loans that do not meet those requirements are referred to as nonconforming, and sometimes non-qualifying, or NQ.

If a mortgage has an interest-only provision, it will be a nonconforming loan. That means rather than being funded by Fannie Mae or Freddie Mac, it will be funded by a non-agency lender. This is typically a bank or other financial institution that provides loan funds out of its own portfolio.

Since the loans are provided by direct lenders, those lenders can set their own lending criteria and requirements. They can be very different from those on conforming loans.

As a general rule, interest-only loans are available only to highly qualified borrowers. That will mean good or excellent credit, a down payment of 20% or more, and alow debt-to-income ratio (below 43%).

Who Offers Interest-Only Mortgages?

Because interest-only mortgages are nonconforming (or nonqualified, or NQ) loans, the number of lenders where they’re available is extremely limited.

We were able to identify four such lenders. The programs are designed primarily for larger loan types, and typically require higher down payments than will be the case with conventional loans.

Specific information, as well as pricing data, isn’t provided by any of the four lenders. Each invites you to make an application online or to contact a company representative for complete details. While that may not be convenient, it’s probably the best strategy, given the unique features of interest-only loans.

Key Bank

Key Bank offers two different interest-only mortgage programs, Gold Key Interest-Only and Jumbo Interest-Only.

Gold Key Interest-Only is a program designed only for Key Private Bank and Key Family Wealth clients. It’s available in loan amounts ranging from $548,251 to $3.5 million, with a minimum down payment of 20%. It’s a 30-year loan program that’s interest-only for the first 10 years. It’s a variable rate program that comes in 10 year/6 month, 7 year/ 6 month and 5 year/6 month terms.

Jumbo Interest-Only is similar, except that it doesn’t require Key Private Bank or Key Family Wealth status. It has the same loan limits, a 10-year interest-only period and variable rate terms. But it’s limited to no more than 70% of $1.5 million for a primary residence, or up to 65% of $2 million for second homes. You must have an eligible KeyBank checking and savings account to qualify.

For either program, the property must either be owner-occupied or a second home. Availability is for single-family homes, condominiums, or homes located in planned unit developments.

Griffin Funding

Griffin Funding offers their Interest Only Mortgage program. It’s available in both 30-year and 40-year fixed rate loans, as well as 7/1 and 5/1 adjustable-rate mortgages. Interest only is due in the first 10 years of the loan. These are considered non-qualifying loans, available primarily for residential and commercial real estate investors.

The website doesn’t provide specific interest rates or qualification requirements, so you’ll need to request an online quote or speak with a company loan officer.

New American Funding

New American Funding only indicates that they offer interest-only mortgages, with the interest-only feature applied for the first 5 to 10 years. To get more information, you’ll need to submit an online application.

Homebridge Financial

Homebridge Financial offers an interest-only payment option with their Investor Cash Flow program. It’s a fixed rate program with a 30-year term, including 10 years interest only. But it’s also available with adjustable rates as either a 10 year/6 month or 7 year/6 month term.

Loan amounts and down payment requirements are determined by the specific income qualification method you choose (since it’s a non-qualified mortgage, income can be fully documented, based on investor cash flow, or on bank statements).

However, it appears Homebridge Financial is a mortgage wholesaler, and not a direct lender. Contact the company to learn which mortgage providers offer their interest-only program in your area.

Pros and Cons of Interest-Only Mortgages

Pros

Lower monthly payments – borrowers can save hundreds of dollars per month with no principal payment requirement.

The lower monthly payment may enable you to qualify for a larger mortgage, and therefore a higher-priced home.

You can lower the monthly payment by making a lump sum prepayment on the mortgage. Since interest is calculated based on the loan balance, the interest payment will decline with each prepayment of principal.

Loan qualification may be more flexible. This is because interest-only loans are available from direct lenders, and not subject to mortgage agency guidelines.

Cons

Payment shock. As the example in this guide shows, your monthly payment can increase by more than 150% once principal payments begin.

Lack of equity buildup. You’ll be relying entirely on price appreciation to build equity. If your property doesn’t appreciate, you won’t build equity. And even if it does, the equity buildup won’t be as quick as it would be with a fully amortizing loan.

Because of the lack of equity buildup, you may be unable to sell or refinance the property if it doesn’t rise in value.

Fewer choices. Since these loans are offered by only a handful of lenders, and often only under certain very limited circumstances, there may be no more than one or two lenders available to you.

The lack of equity buildup may make it more difficult to get secondary financing later, from a home equity loan or home equity line of credit.

You could be stuck with the loan if interest rates rise, and you’re unable to qualify for a refinance, or if you remain in the property past the interest-only period.

Summary

Interest-only mortgages are a highly specialized loan type designed for very specific borrowers. Because they are higher risk loans, you should consider one only if the benefits are clear, and you can qualify for the program with room to spare. These are not the type of loans for borrowers with minimum down payments, tight income qualifications, or borderline credit profiles.

And most of all, you should be reasonably certain you’ll sell the home before the interest-only period expires. If not, you’ll be dealing with all the negative aspects that keep interest-only loans from being offered by more lenders.

Ask An Expert: When is an Interest-Only Mortgage a Good Idea?

As a general rule, you should only consider an interest-only mortgage if you’re well-qualified, and you expect to sell the home within the interest-only time period. “Well-qualified” refers to having above average credit, a debt-to-income ratio that’s well within program requirements, and a down payment of at least 20%.

An interest-only mortgage may also be a good option if you expect to be in a position to repay a substantial portion of the mortgage balance during the interest-only phase of the loan. If you can, the impact of the transition to full interest and principal payments will be lower, since they’ll be calculated based on a lower loan balance.

Even if you qualify and plan to sell within the interest-only timeframe, you should still carefully consider the potential problems with slower equity buildup, as well as the possibility you may remain in the home longer than expected.

Either situation could limit your options to either sell or refinance the property, which is the primary reason why the major mortgage agencies, like Fannie Mae and Freddie Mac, eliminated interest-only mortgages after the global financial meltdown.