HELOC (or Home Equity Line of Credit) vs. a home equity loan - which is the right choice for you? In truth, the two loan types represent two versions of the same financing arrangement: each enables you to access the equity in your home without the need to take a new first mortgage.

What makes a HELOC and a home equity loan attractive is that the funds can be used for just about any purpose, without requiring the homeowner to apply for a new, larger first mortgage.

However, each loan type accomplishes that goal in a somewhat different way. The good news is that you can choose the financing arrangement that will best accomplish your goals while fitting comfortably in your budget.

How to Calculate Your Home Equity

The common words in both loan types are 'home equity.' That is, each represents a draw against the equity you have in your home.

How do you calculate your home equity?

The first task is to determine the value of your home. Though this will ultimately be done through an appraisal performed by the lender, you can get a ballpark valuation from free websites like Realtor.com and Zillow.

Let's say you determine your home has a fair market value of $300,000. Whether you are applying for a HELOC or a home equity loan, the lender will typically allow you to access up to 80%-85% of that value, depending on their lending policies.

At the high end of the range, the lender will give you access to up to $255,000 ($300,000 X 85%) of your home's value. But they'll first subtract the amount of any existing loans on the home.

If you already have a $200,000 first mortgage on the property, the maximum HELOC or home equity loan the lender will make will be $55,000 ($255,000 − $200,000).

The home equity calculation will look like this:

Applying that calculation to the example above will look like this:

($300,000 X 85%) − $200,000 (existing first mortgage) = $55,000

Can You Have More than One HELOC or Home Equity Loan?

In theory, at least, it's possible to have more than one HELOC or home equity loan on your home. However, in practice, a traditional lender will be unlikely to provide you with an additional HELOC or home equity loan.

The existence of the first mortgage, plus an existing HELOC or home equity loan, means any additional loan arrangement will be in the third priority, behind the first mortgage and the first HELOC/home equity loan.

That means if you were to default on your payments, the provider of the second HELOC or home equity loan would only be paid out of the proceeds of the foreclosure of the home after the first mortgage and the first HELOC/home equity loan have been satisfied.

If you already have a HELOC or home equity loan on your home in addition to a first mortgage, and apply for another, the new lender will almost certainly require you to replace the original HELOC/home equity loan with a new, larger one. That will enable the lender to maintain second priority behind the first mortgage.

What is a Home Equity Line of Credit (HELOC)?

Perhaps the best way to describe a home equity line of credit is to think of it as a credit card secured by your home equity.

That's a very general description since there are significant differences between a HELOC and a credit card.

Carrying the example forward, a HELOC would be set up as a $55,000 line of credit against your home equity.

Below are the basic terms of a HELOC.

Accessing Your HELOC

Once your home equity line of credit is in place, you can access the loan when funds are needed, and in any amount, up to the maximum line. And as you repay the amount borrowed, you'll be restoring the line for additional borrowing.

However, accessing a HELOC is only permitted during what is known as the draw period. That's a specific amount of time you'll be allowed to draw on the HELOC, after which additional access will not be permitted.

The draw period is typically five or 10 years, and usually not more than 50% of the loan term. For example, a HELOC may have a 10-year draw period, followed by a 20-year repayment term. In this case, the total loan term would extend out to 30 years, with 10 years for the draw, and 20 for the repayment.

Repaying Your HELOC Balance

The reason there is a limited draw period on a HELOC is to give you time to repay the money you borrowed.

During the draw period, you'll be required to pay only interest on the amount of the line that's outstanding. For example, if $20,000 of the HELOC is outstanding, and the interest rate is 6%, you'll make monthly interest payments of $100 ($20,000 X 6% = $1,200 divided by 12 months).

Naturally, the amount of interest you'll pay each month will vary based on the amount of the line that's outstanding and the applicable interest rate at the time.

But once the draw period ends, you'll be required to make monthly payments that include both interest and principal repayment.

Two features a HELOC has in common with a credit card are variable rates and monthly payments.

The interest rate will be calculated based on an index, plus a margin. The index might be the prime rate, with a margin of 1% added to it. For example, with the prime rate at 3.25% and a 1% margin added, the result will be a loan rate of 4.25%.

The rate can adjust, higher or lower, based on changes in the prime rate. However, the exact amount of the margin -- and your applicable interest rate -- will also depend on your credit history, income, debt-to-income ratios, and the amount of the HELOC.

That said, your HELOC may come with a low introductory rate. For example, even though the fully indexed rate may be 4.25%, the lender may offer you 2.99% for the first 12 months. They'll do this to entice you to take their HELOC over one offered by a competitor.

You should also know the variable feature for both the interest rate and monthly payment will continue throughout the repayment phase. Both will be adjusted, higher or lower, based on changes in the prime rate.

What is a Home Equity Loan?

Though both a HELOC and a home equity loan enable you to tap the equity in your home, exactly how each does it and their repayment terms are where these two loan types go in different directions.

While a HELOC is a line of credit against your home, a home equity loan is an outright loan. For this reason, home equity loans are frequently referred to as second mortgages.

Accessing Your Home Equity Loan

Unlike a HELOC, where you can access your credit line as you need funds, a home equity loan gives you all the proceeds upfront. If the loan amount is determined to be $55,000, the funds will be provided to you immediately.

Repaying Your Home Equity Loan Balance

Just as you will receive the proceeds of your home equity loan immediately, you'll also be required to begin making regular monthly payments.

Home equity loans are available in terms ranging from five years to as long as 30 years. Much like a first mortgage, you'll be making monthly payments over the full term of the home equity loan.

Fixed Interest Rate and Payment

While HELOCs come with variable rates and payments, home equity loans have fixed rates and payments.

Much like HELOCs, the interest rate on a home equity loan will be determined by a combination of your credit history, income, debt-to-income ratio, and loan amount. As a general rule, the average rate on home equity loans is higher than it is on HELOCs.

If you borrow $55,000 on a home equity loan with a 20-year term and a 4.25% interest rate, your monthly payment will be $340.58.

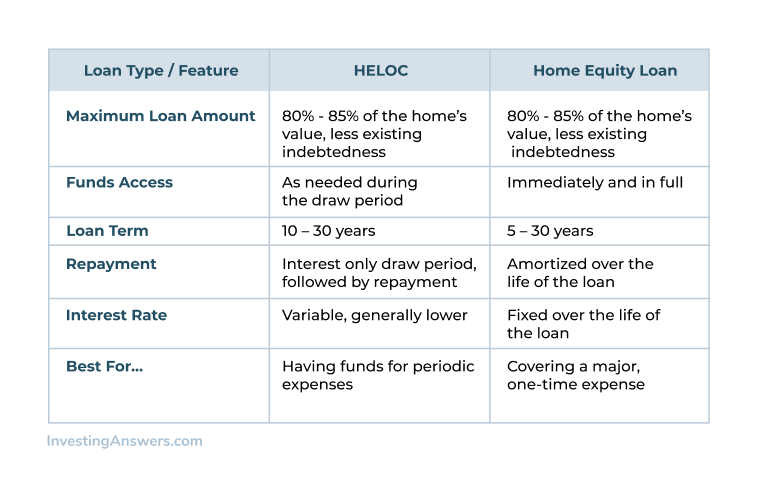

HELOC vs Home Equity Loan

The table below summarizes the similarities and differences of HELOCs vs. home equity loans:

HELOC vs. Home Equity Loan – Tax Considerations

Whether you take a HELOC or a home equity loan, the tax-deductibility of the interest on either financing arrangement is the same.

Under current IRS regulations, the interest on secondary financing secured by your home can be claimed as a deduction under the following two circumstances:

1. The loan proceeds are used to substantially improve your home, and 2. When the loan amount, when added to the first mortgage, doesn't exceed $750,000.

Based on those rules, if you take a HELOC or a home equity loan and use the proceeds to make an addition to your home, the interest on the financing will be tax-deductible as long as the total indebtedness on your home doesn't exceed $750,000.

But if the proceeds were used instead for debt consolidation of credit cards and a car loan, no deduction will be permitted.

How to Choose HELOC vs Home Equity Loan

Whether you choose a HELOC or a home equity loan will depend on your own needs and repayment preferences.

A HELOC will be a better choice if:

You expect to have an ongoing need for extra cash as major expenses arise.

You're looking for the lowest interest rate possible, particularly in the early years of the loan.

The variable-rate feature of a HELOC doesn't disturb you.

You have no immediate need for financing but want a credit line to tap into as a supplement to your emergency savings.

Though you expect to have major expenses in the future, you're equally confident you'll be able to pay off your loan draws quickly thereafter, minimizing your interest expense.

You're not interested in a long-term monthly payment commitment.

A home equity loan will be a better choice for you if:

You have an immediate need to cover a major expense, like remodeling your home.

You prefer the predictability of a fixed interest rate and monthly payment.

You're interested in consolidating a large amount of variable-rate debt, like credit cards, into a single fixed payment, fixed-term loan arrangement.

You plan to stay in your home for many years.

Summary

Both HELOCs and home equity loans are secured by your home and the amount available is determined by how much equity you have in your home.

Choosing whether a HELOC or home equity loan is right for you will mostly come down to when you need the money. If you need the full amount right away then you should consider a home equity loan. However, if you want access to funds but will need smaller amounts overtime then a HELOC may be a better fit.